Second Half Market Settling

The Southeast Michigan housing market is entering fall with mixed signals, pointing toward a gradual cooling but continued strength in values.

Through August, sales are down 1% compared to 2024, while new listings slipped 6%. Inventory is up 10% year-over-year, but quality listings remain scarce in relation to demand. The imbalance continues to drive prices. Average sale prices have climbed 5% year-to-date to $352,363, reflecting strong buyer demand even as activity slows.

Looking forward, several leading indicators suggest the market will moderate as we head into the final quarter.

Pending sales peaked in June and have been tapering since, a seasonal pattern that often signals softer closed sales numbers in the months ahead.

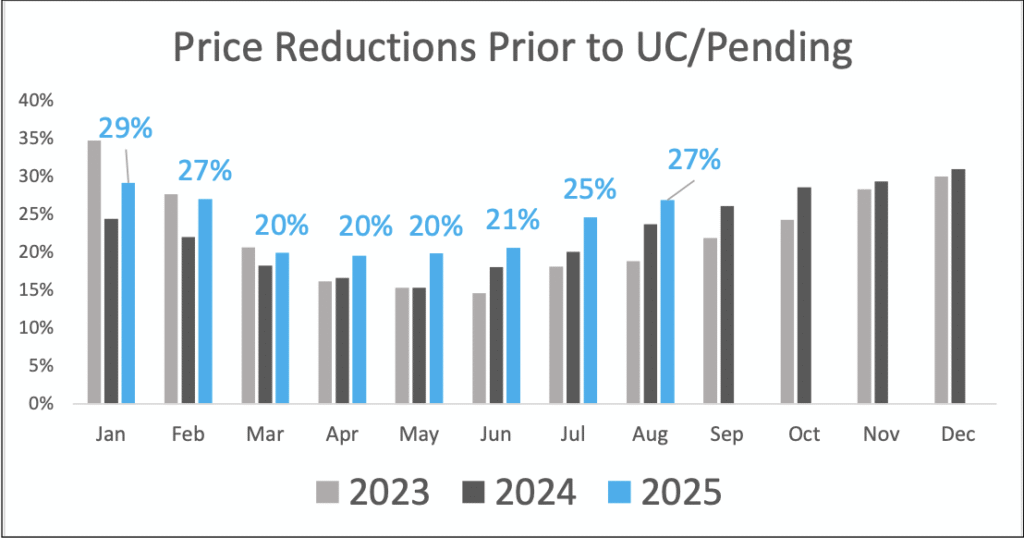

Price reductions are on the rise after bottoming in May, an early sign that sellers may need to temper expectations as buyer urgency is moderating.

While 57% of August closings were still at or above asking price, that share has been steadily drifting down from the 60–65% levels seen over the past two years. The competitive edge remains, but intensity is easing. Homes selling in under 10 days peaked at 53% in early summer; that figure is expected to decline through year-end, giving buyers a bit more breathing room.

Prediction: The balance of 2025 will likely bring fewer bidding wars, longer market times, and a slight rise in inventory as new listings and price reductions intersect.

Buyers may see modestly more leverage, but continued tight supply of quality listings should keep values elevated. Expect more price reductions and longer market times for homes in average or below average condition.

In short, expect a market that leans toward sellers — but with less heat than the spring and early summer peaks.