SE MI Market: Solid and Steady

The Southeast Michigan market continued its gradual path toward normalization through October, with seasonal cooling in new listings and pendings but solid pricing and stable year-to-date performance. While activity has leveled off since mid-summer, the broader 2025 trend for the region remains defined by rising values, and steady demand.

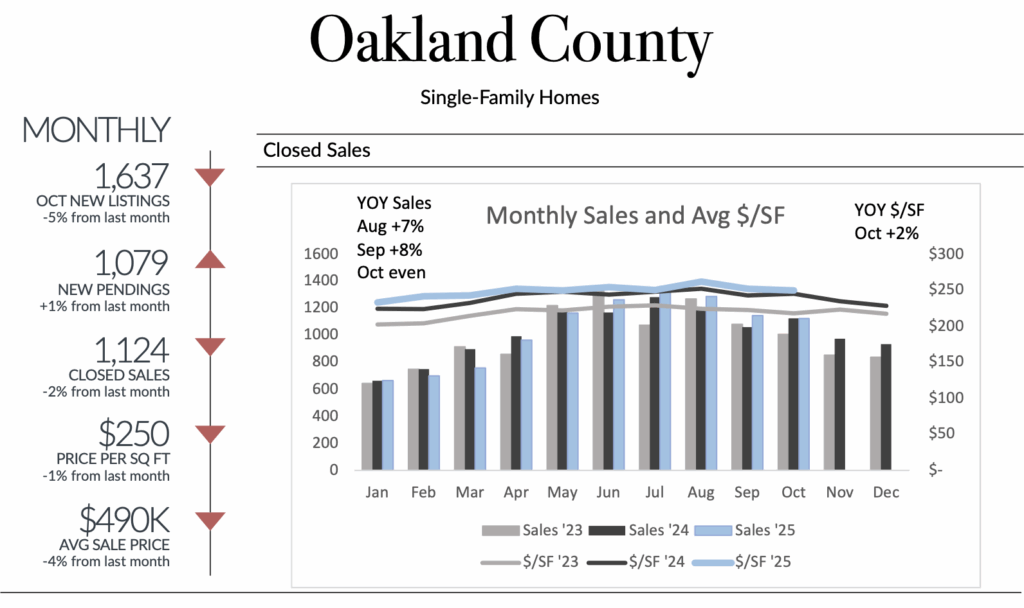

Sales & Market Activity

Year-to-date sales are essentially even with 2024—down just 1%—despite fewer new listings entering the market. Monthly pending activity peaked in June and has eased each month since, with October pendings landing 1% above last year but below long-term norms. Buyers remain active, but they’re moving more deliberately than during the pandemic-era cycles.

Values & Price Trends

Pricing remains a consistent bright spot. Average sale price is up 5% YTD and $/SF is up 4%. That 5% average, however, is slightly misleading in that it’s caused in part by a 9% increase in upper-end “over $400k” sales. Within any price level (including upper-end sales), prices are up two or three percent. But the main value takeaway is that the pricing trend remains stable and positive.

Inventory & New Listings

Sellers continue to participate at restrained levels compared to last year. New listings are down 5% YTD and 11% YOY in October alone, marking the third consecutive year of reduced seller activity in the fall months.

Shifts in Market Dynamics

Market mechanics continue to normalize toward pre-2020 patterns.

•53% of October closings sold at or above asking, down from earlier in the year and trailing 2023–24 norms.

•Price reductions rose to 32% of October pendings, signaling increasing selectiveness among buyers.

•DOM has been rising since June, moving from the mid-20s to the low-30s by October.

•The share of homes going pending within 10 days has eased to 40%, down from this year’s peak of 53%.

These indicators reflect a marketplace that still favors sellers but no longer operates at the hyper-competitive pace of the past several years.

Looking Ahead

As we head toward year-end, local markets remain fundamentally strong. Expect a temporary easing of average prices—a reflection of picked-over year end inventory. But the market remains healthy, and sales are tracking nearly even with last year. With demand stable and inventory constrained, early 2026 is likely to open with similar conditions: competitive for the best listings, more price-sensitive for mid-range and dated inventory, and generally more balanced than the post-pandemic peaks.