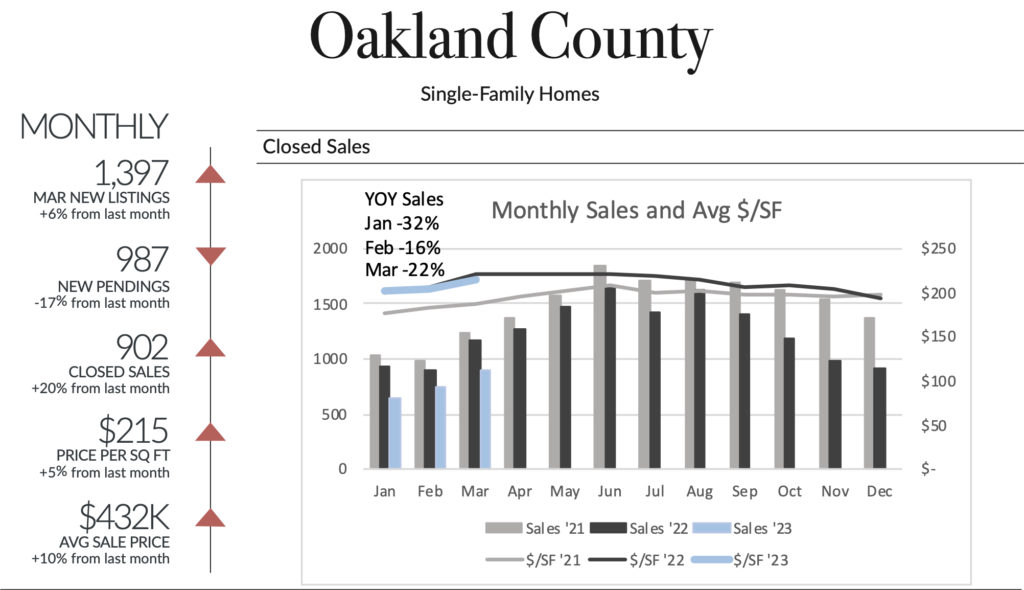

The first quarter kept everyone guessing as to how 2023 was going to play out. Coming off of the past two years of pandemic-induced demand, everyone expected demand to ease and the market to cool off by a few degrees.

While closed sales faded fifteen to twenty percent compared to the past two extreme years, demand remains remarkably strong with buyers waiting and watching closely for the right new listing to arrive. Prices are generally about even with they were last year—over 30% higher than they were pre-pandemic.

The frequency of quick sales at or above listing price is rising and the frequency of price reductions is falling. While we won’t be able to keep up with the pace of ’21 and ’22 sales, the bottleneck isn’t in lack of demand, but rather the limited availability of quality listings. The market is stable and it continues to be a great time to sell.

Sales Limited by Supply

Thirst for Quality Homes Remains Unquenched

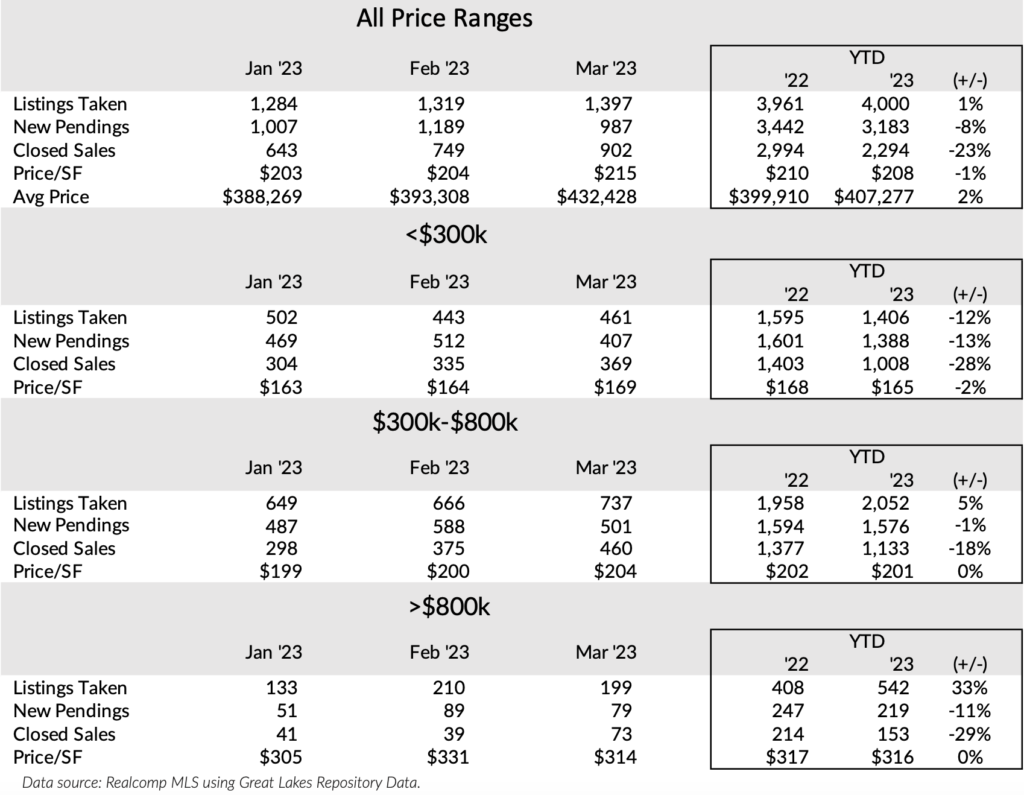

Despite continued strong demand, limited active inventory quantity and quality continues to bottleneck sales. Although March closed sales were up 26% compared to the prior month, a 10% drop in March new pendings will limit April closed sales.

The best listings continue to sell quickly—42% of March new sales and half of April’s (through April 17th) took 10 days or less. Quality and quantity on the supply side seem to be limiting sales more than any lack of demand.

Thirty-five percent of March closed sales were above full asking price, 18% were at asking and less than half were under. As shown in the “Under, At and Over” chart, the “Over” sales are increasing while the “Under” sales are decreasing. Expect the Over-Asking percent to peak in June as it has done the past two years.